📦 Cajas Populares

Millions of microbusinesses run on family loans, supplier credit, and savings circles. A cooperative movement helps fill the gap.

We create custom data stories for global companies that want to reach Latin America's business community — the same kind of content you're about to read below, but built around your industry expertise and distributed to our 300K+ audience. If that sounds interesting (for you or someone you know), let's talk to see if we're a good fit. [Schedule 15 minutes →]

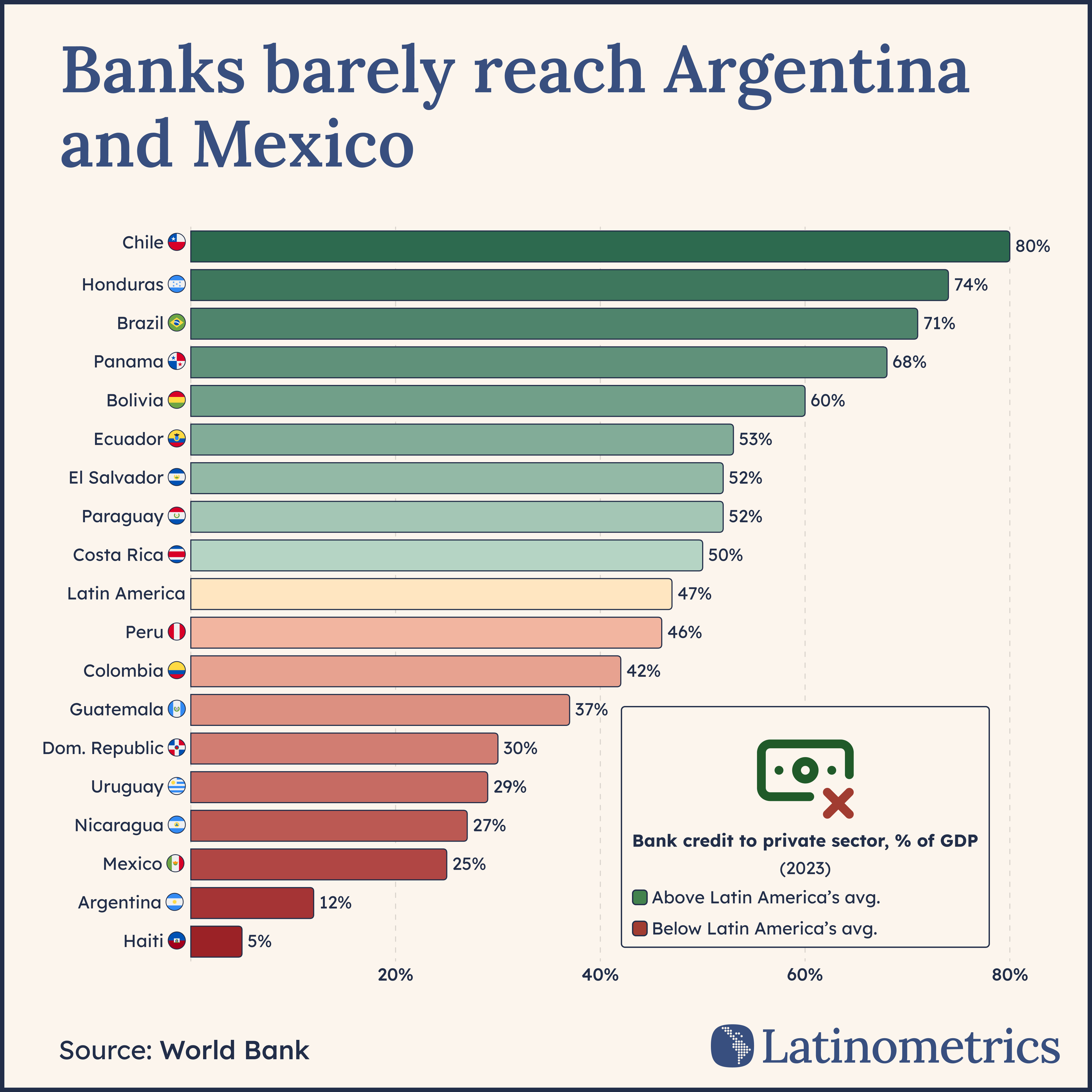

Longtime Latinometrics readers know we once called Brazil the banking capital of Latin America, a title the country earned through its mix of massive century-old banking giants, the region’s largest, alongside innovative new fintech disruptors.

Well if Brazil is the center of the region’s financial map, then Mexico is the remote mythical island of which sailors speak in legends.

After all, Latin America’s second-largest economy possesses a uniquely peculiar financial landscape, one in which the domestic private-sector credit offerings more closely resembles far more troubled economies like Argentina or Nicaragua than more traditional peers like Brazil or Chile.

On average, Mexican businesses can obtain half the credit as a percentage of GDP (25%) than their peers across the rest of Latin America at 47%. That financing gap alone explains why the Mexican economy continues to run on self-finance, family loans, supplier credit, informal savings…really, everything other than the formal banking system.

If you think this minimal credit depth is just some obscure macro problem for economists in Mexico City to sweat over, guess again.

Only 10% of businesses obtained any financing in 2023, a low figure that’s actually down from the over 12% seen in 2018, meaning the overwhelming majority of Mexican companies are operating without outside credit.

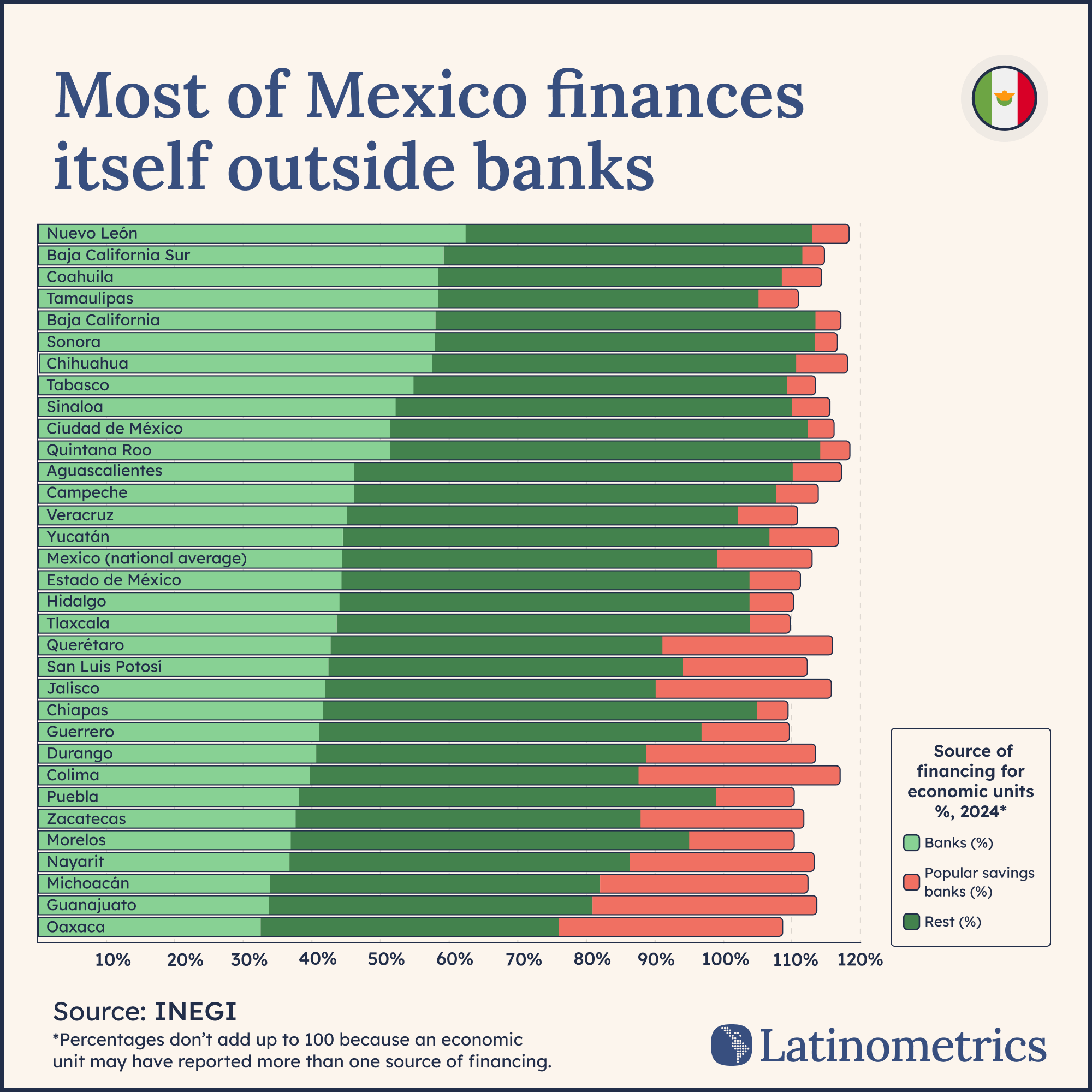

Even if you were among the lucky few to get some financing, you likely didn’t turn to your friends at BBVA or Banamex for it. Among the roughly one-in-ten businesses that secured financing, less than half (44.4% to be precise) used bank credit, while the rest turned to other channels.

Evidently, to speak of Mexico’s financial sector is really to speak of two systems: a formal one that serves larger, more established companies, and another one that cobbles together piecemeal credit options for everyone else as best it can.

In this tale of two credits, the size of your company helps determine which system you operate in.

Over 95% of companies in the country are microbusinesses, yet barely 4.5% of them accessed bank credit. To contrast, roughly a third (32%) of large firms obtained financing, indicating that established finance tends to accompany those companies with the right scale, paperwork, and above all formality.

Naturally, once we’re talking business formality you’ll find that the divide maps on pretty well to Mexico’s greater schisms surrounding economic opportunities and income inequality. Nearly 65% of businesses are informal in the country today, up from 62% a few years ago.

These businesses generate 8.6x less income per worker than their formal peers, reinforcing a vicious cycle in which low productivity limits formal finance—and lack of finance constrains productivity.

Which isn’t to say this is a problem reserved for the private sector. Among surveyed Mexicans, over a third (37%) saved exclusively through informal means, one in five (20%) participated in tandas (informal rotating savings circles), and nearly three in ten (29%) used informal credit. Evidently, for tens of millions of people, finance takes place outside of Banco Azteca’s doors.

And as with most other economic gaps, women are especially exposed to this lack of finance, given they make up 54% of informal workers versus 40% in formal firms.

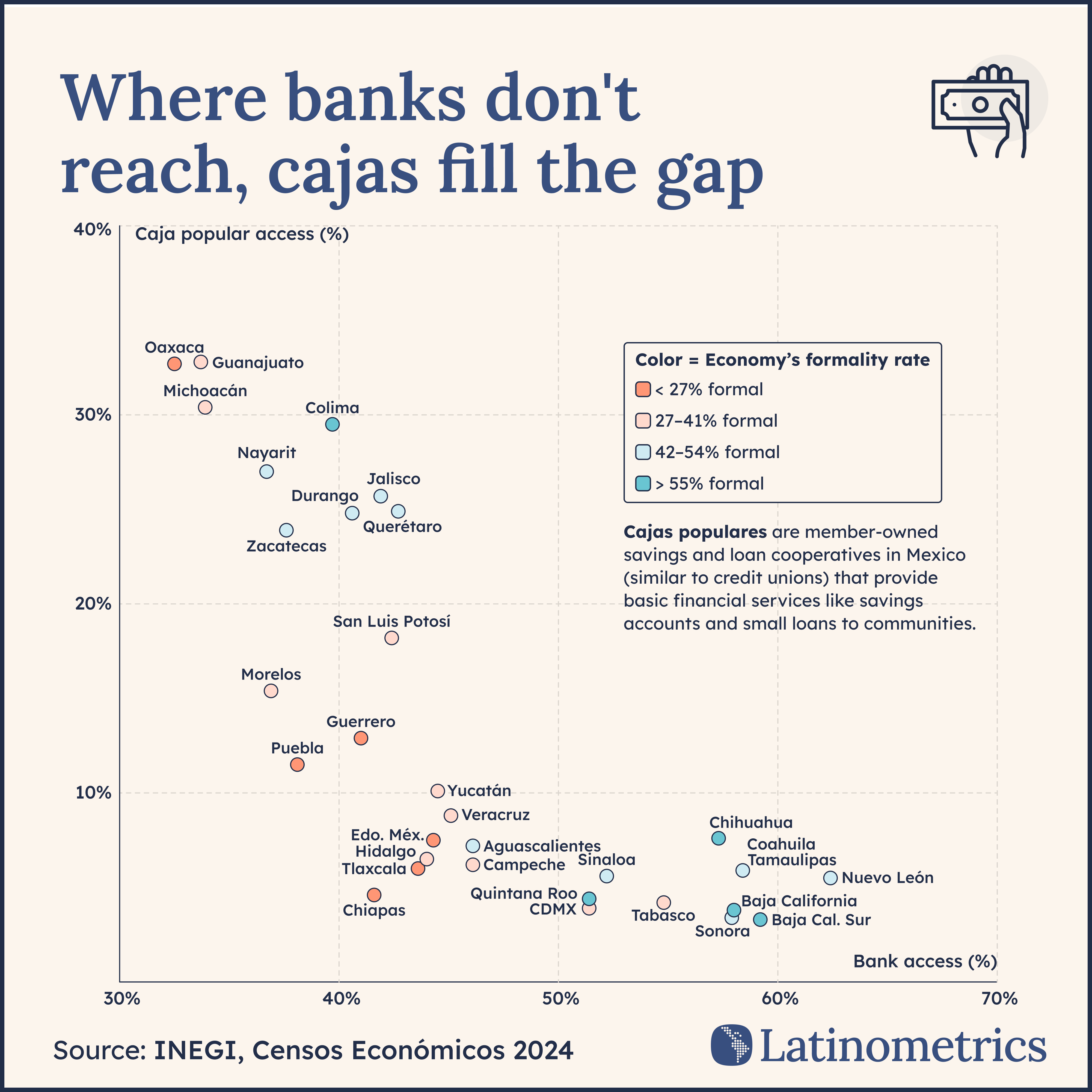

Does the severity of the problem depend in part on where you live? For that, just look to a map. Financed businesses in northern states like Nuevo León are turning to banks to a degree of double their peers in states like Oaxaca. In fact, in the latter case, cajas populares are actually more utilized.

These cajas, or cooperative savings banks, have soared in popularity in recent years. They number over 140 in Mexico today, serving more than 8.6M members across roughly half of the country’s municipalities.

Their total assets grew by 457% between 2010 and 2022, while the largest of them today, Caja Popular Mexicana in León, has grown into Latin America’s largest credit union, with roughly 3.4M members across nearly 500 branches in 22 states.

Which serves as a key reminder: global economic history has long been shaped by financing solutions stepping up to address corporate and industrial needs, from the joint stock companies and crédit mobiliers of the mid-1800s to the investment banks of the last century. Cajas populares serve as a contemporary example.

Today, Mexico’s two financial systems transcend debates of formality to encompass geographic and social elements, with a more banked north, a more cooperative south, and millions of Mexicans and companies still operating without access to reliable credit. Where the banks don’t reach, Mexicans have built a second financial architecture to compensate.

Comment of the Week 🗣️

Edward tells his story of growing up with the maquiladoras in Juarez, Chihuahua. “Cheap labor, alone, should never be the end desire or result of foreign trade.” Well said.

Feedback or chart suggestions? Reply to this email, and let us know!