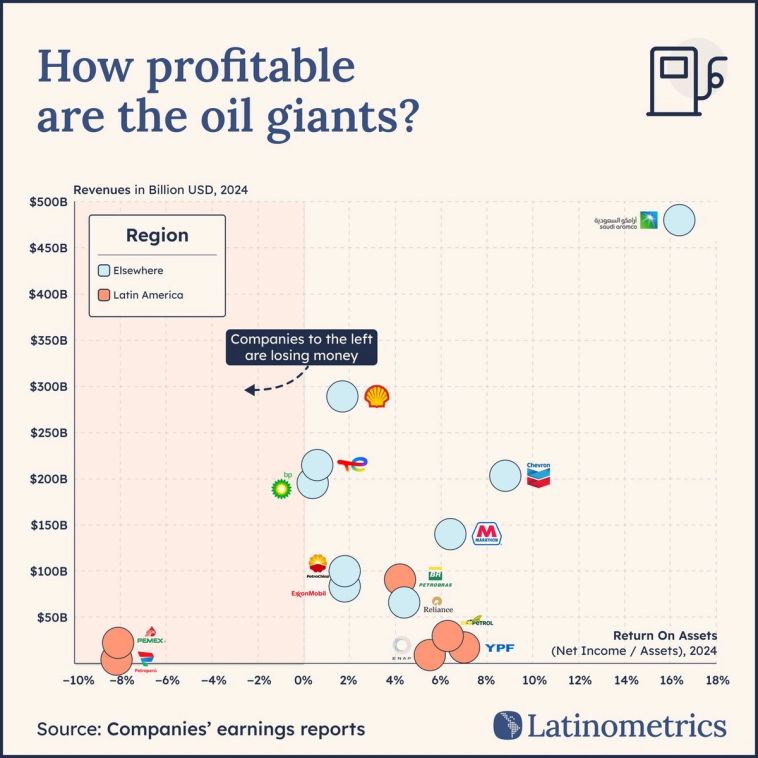

Pemex has some concerning debts

How do the world's top oil producers compare in performance?

It’s the oldest debate in Latin America: just how much state presence is good for the economy?

Most modern economists agree that too much of a state role in guiding or managing a national economy can be fatal, as seen in historical examples like the Soviet Union or contemporary regional examples like Cuba and Venezuela. Too little presence, and it can be hard to rally aggregate demand or keep inflation low.

Unfortunately, these can have their own issues, as the case of Pemex can illustrate. Formed in 1938 after the nationalization of Mexico’s oil industry, Pemex has long been plagued by issues relating to government management. Just this week, in fact, the world’s largest sovereign wealth fund divested its Pemex position over decades of corruption scandals.

Part of the problem is that, by having government at the table, SOEs can have market-irrational tendencies foisted upon them. Petrobras, for example, has long needed to keep domestic gas prices artificially low in order to spare the Brazilian government from the wrath of the powerful truckers’ union, which famously went on strike in June 2018.

In the case of Pemex, meanwhile, profits have often been redirected elsewhere. The company pays out over half of its annual revenues in taxes and royalties, making up roughly a third of all tax revenue collected by Mexico. Good for the federal budget—not so much for firm operations. No wonder Mexico’s production has cratered and even New Mexico outproduces it now.

In recent years Pemex has been called the most indebted oil company worldwide. Only Petroperú, its far smaller Peruvian counterpart, is in such bad shape. Meanwhile, peer SOEs in Argentina, Chile, and Colombia are doing much better fiscally.

Just over a century ago, Argentina’s YPF was founded as the world’s first oil SOE outside of the Soviet Union. The firm was privatized in the 1990s, then renationalized in 2012, and now expected to be reprivatized shortly under the Milei administration.

Is such a liberalization push the secret to ending Pemex’s money woes? Would less government interference save the company? It’s worth noting that the world’s top oil firm, Saudi Aramco, is an SOE, while only one of the following private supermajors – BP, or British Petroleum – was in the red last year.

Getting the Zocalo out of Pemex corporate affairs may just save the firm. But as controversies swirl around YPF and Petrobras, Latin America’s key debate on the role of the state in the economy will clearly persist.