How much GDP is there to manage by bank?

A low-density system won the margin game; the next advantage is winning mass inclusion.

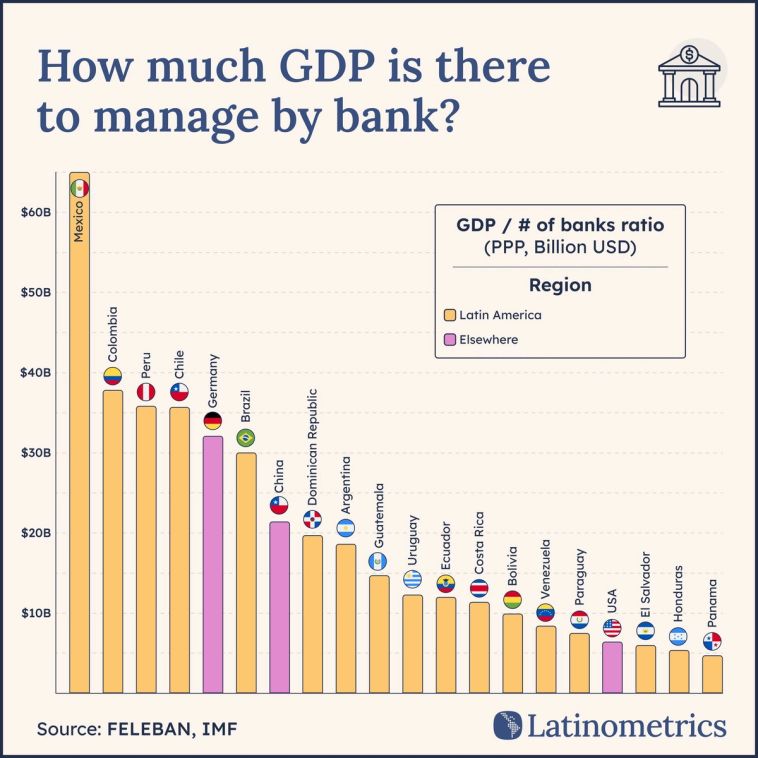

We once noted that Brazil is the banking capital of Latin America. Yet when it comes to the ratio between market size and banks, Mexico is the place to watch.

Latin America’s second-largest economy towers above its peers on gross domestic product per bank, with a staggering $60B of GDP managed per institution.

On paper, that looks like efficiency: fewer banks handling more of the economy. But scratch deeper, and it represents more than just “low bank density.” It points to a system that is both concentrated and at times downright exclusionary.

Meanwhile, private credit is stuck at 31% of GDP, less than half the OECD average. That all points to big banks with narrow reach: lean on the surface, shallow underneath.

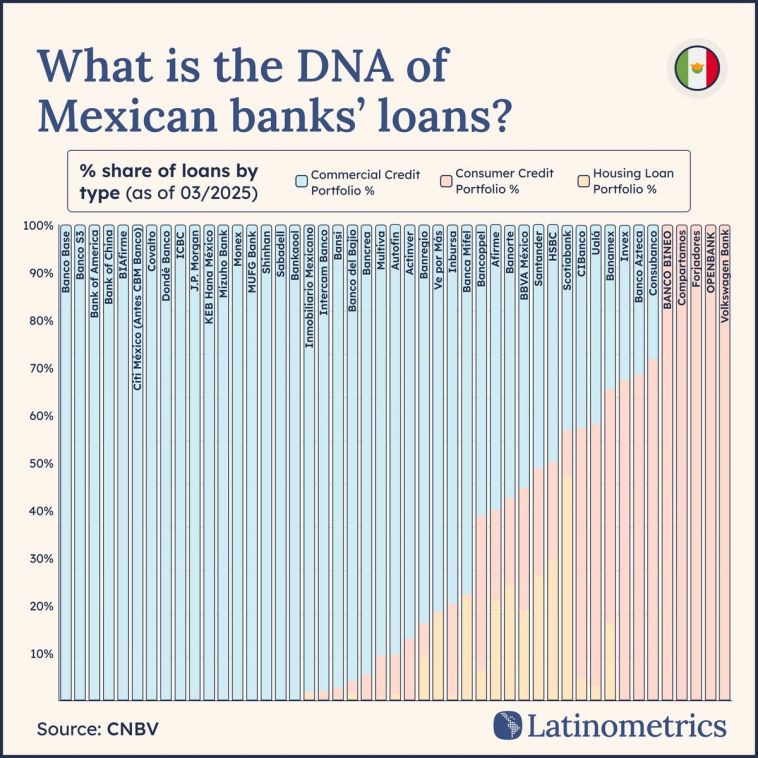

So what do Mexican banks do with their lending firepower?

The loan mix says it all: they’re overwhelmingly tilted toward commercial credit. Consumer and housing loans play second fiddle, meaning firms and corporate clients enjoy easier access while households are left on the margins. That helps business investment, but it reinforces gaps in financial inclusion.

The exclusion is stark. A whopping 51M of Mexicans—about half the population—remain unbanked. In practice, banks are serving the formal sector well, while the informal economy and lower-income groups remain credit-starved. It’s a structure that stabilizes earnings at the price of an under-stimulated domestic market.

The paradox is that when banks do lean into consumer finance, growth is explosive. Banorte’s loan book swelled 13% year-on-year in Q2 2025, with auto loans up 30% and credit cards up 18%. Profitability soared to 23.6% ROE while non-performing loans held at just 1.1%. Clearly, appetite exists when banks push into households.

Economists remain divided overall, however. The OECD argues that financial deepening (namely, expanding accounts and private credit) is essential to cut inequality and drive growth. Others say Mexico’s concentrated model is exactly why its banks stay profitable and resilient. The bigger question looms: will banks remain comfortable as corporate financiers, or pivot toward true mass inclusion?

The answer could shape not just their balance sheets, and their insulation against the rising fintech challenge, but also Mexico’s long-term growth story.

Fintechs will win

Old banks will win

On US citizens living in Mexico.