Small countries carry LatAm's heaviest debt loads

Why Latin America is better at paying off debt than most developed countries.

Do you remember where you were in 2019? Were you starting a new job, maybe saving up for a down payment on a house or entering a relationship?

If you're anything like us, late 2019 was all about setting goals and looking ahead to the following year with big dreams—while 2020 was all about watching a virus upend the whole planet and force you to mask up for all your plans.

Above all, the COVID shock was felt economically, with lockdowns and outbreaks leading to a worldwide standstill. The S&P 500 dropped by 16% within a week. The price of oil became negative. The global economy contracted by 3%, while in Latin America this figure looked closer to 7-8%.

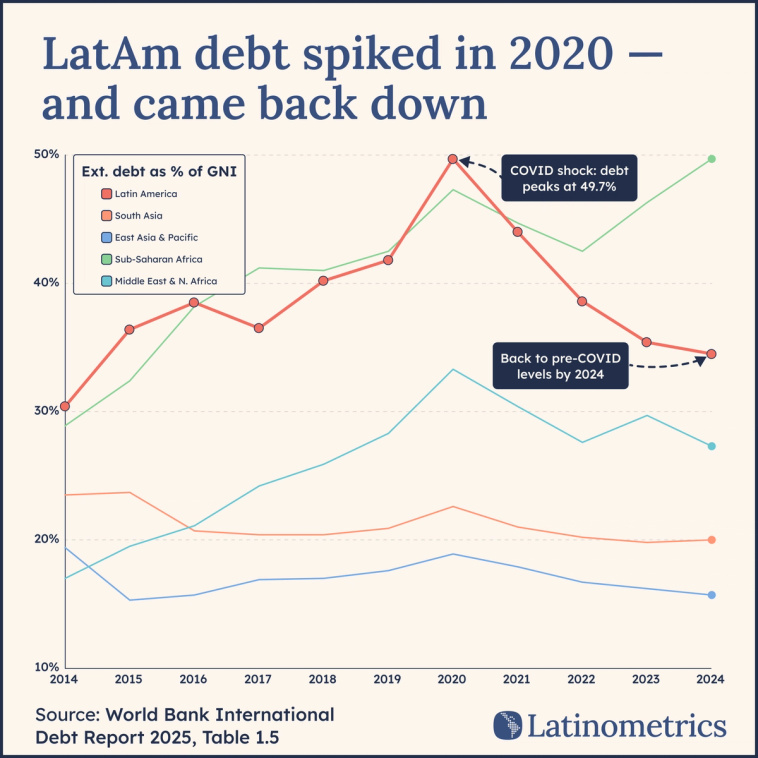

Accordingly, same as people or businesses, governments borrowed money to get through this tough period. Regional debt, which had already climbed from 30% to 40% of gross national income since 2014, spiked to nearly 50% in a single year.

Notably, there were divergences within the region, with Mexico's then-president emerging as a fiscal hawk while more generous social policies were passed in both Argentina and Brazil.

But more remarkable in the post-COVID era is how Latin America as a whole has been able to reduce debts since the pandemic. While France and Italy spend 3-6% more each year than they take in (and owe over 115% of their annual economic output), to say nothing of the US, Latin American governments have by and large been fiscally disciplined.

The story is partly one of leeway—markets would punish most Latin American governments if they ran up deficits and interest payments like Uncle Sam or the Japanese—and partly one of growth. Recent years' growth has been low to modest, at just 1.6-3% regionally, but still higher than many developed peers.

There are always exceptions. Brazil's high interest payments and fixed public spending have contributed to a stubbornly high deficit, one unlikely to go down during an election year. El Salvador received a $1.4B bailout from the International Monetary Fund last year as it struggles to service its own debt obligations.

On the flip side, Argentina has now posted two consecutive years of budget surpluses, having broadly trimmed public expenditure.

The textbook says governments should save during the good times and spend during the bad ones. Easy to say, harder to do when your voters are hungry and your creditors are watching. The road to reasonable budgets is a balancing act, one that considers the neediest in the country while also not losing credibility in the eyes of those from whom the state will need to borrow.

For a region that spent decades learning hard lessons about debt, maybe the lesson finally stuck.