Paraguay’s FDI grew 12x in three decades

Paraguay's flat tax rate is luring billions from Brazil, Colombia, and the US. Where is it all going?

We create custom data stories for global companies that want to reach Latin America's business community — the same kind of content you're about to read below, but built around your industry expertise and distributed to our 300K+ audience. If that sounds interesting (for you or someone you know), let's talk to see if we're a good fit. [Schedule 15 minutes →]

In a recent story, we dove into the growing popularity of the Asunción Stock Exchange, a 30-year old bourse where local Paraguayan companies access international capital.

Some of you expressed surprise at the mere idea. Investing? In Paraguay?

Yes, Paraguay is what the international investment community would call a frontier market, referring to its status as a developing country with economic and political stability that is too small to qualify as an emerging market like Argentina or Brazil.

But portfolio investment like what’s seen on the Asunción Stock Exchange is not the only sign that Paraguay is shaping up to be an attractive investment destination following its recent upgrades to investment status by S&P and Moody’s. Even businesses are getting the hint.

Foreign direct investment (FDI) into Paraguay has skyrocketed over the last two decades as a result of the country’s relative political and economic stability when compared to neighbors like Argentina and Bolivia.

International companies have turned to Paraguay in search of cheaper labor, macro stability, and access to nearby regional markets through the heart of South America.

They've also been attracted by Paraguay's tax burden, one of the lowest in Latin America given its flat 10% corporate, income, and VAT rates. Brazil's effective corporate rate is 34% (which explains our third chart).

And in a region of boom cycles and electoral push-and-pull, Paraguay's 2.5–3% average annual growth — and stable politics dominated for decades by the same pro-business political party — has only helped.

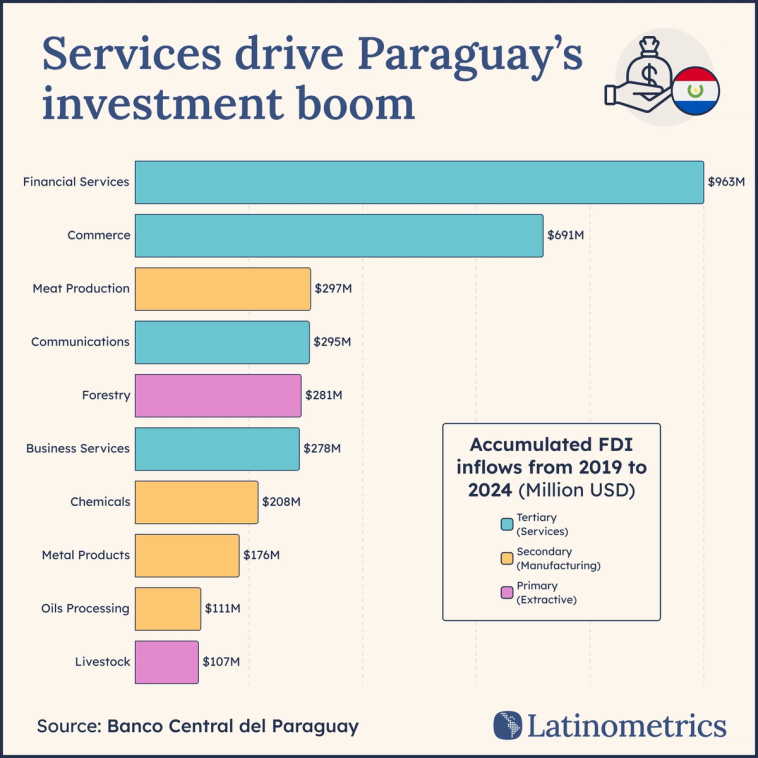

Financial services has emerged as the top sector attracting FDI in recent years, led by examples such as Colombian banking firm Grupo Gilinski’s 2021 acquisition of BBVA Paraguay for $250M.

While total inward finance FDI neared $1B in the 5-year stretch of 2019–2024, commerce served as a clear runner-up with almost $700M in foreign investment. In fact, in the same year as the BBVA acquisition, Brazil’s third-largest energy firm, Raízen, acquired 50% of Paraguayan fuel retailer Barcos y Rodados for over $120M.

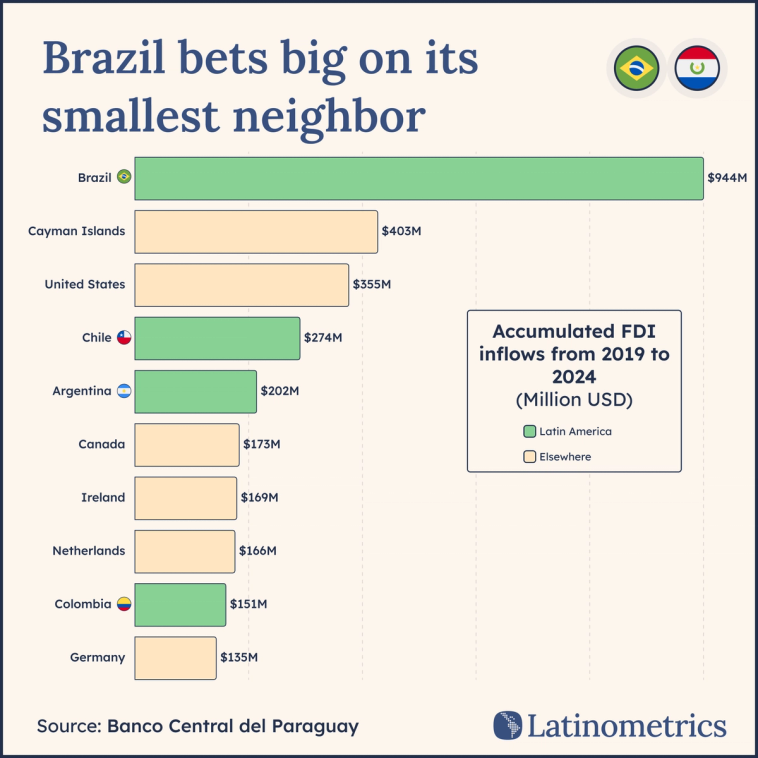

And Raízen is far from alone in going all in on the land of the Guarani. Brazilian firms actually lead the way in investing in their southwestern neighbor, landing ahead of offshore financial centers like the Cayman Islands as well as major investors like the US and Canada.

Beyond the tax appeal and fresh, underdeveloped market, Brazilian companies are often attracted to Paraguay for two main reasons: energy and manufacturing.

On the former front, Paraguay is notable for its cheap energy, on account of producing a surplus in the binational Itaipu Dam sitting on its border with Brazil.

Meanwhile, Paraguayan maquilas (factories that import raw materials duty-free and export finished goods) offer regulatory advantages on tax and capital imports that, coupled with easy exporting to other Mercosur markets, let Brazilian companies boost production while keeping costs low.

As traditional emerging markets like Argentina cycle through crises and Brazil's regulatory costs climb, investors are increasingly looking to the region's smaller, stabler economies for returns. Paraguay may be the most visible example, but it won't be the last.