Latin America holds the minerals everyone wants

China and the US have been scrambling for Latin America's critical minerals.

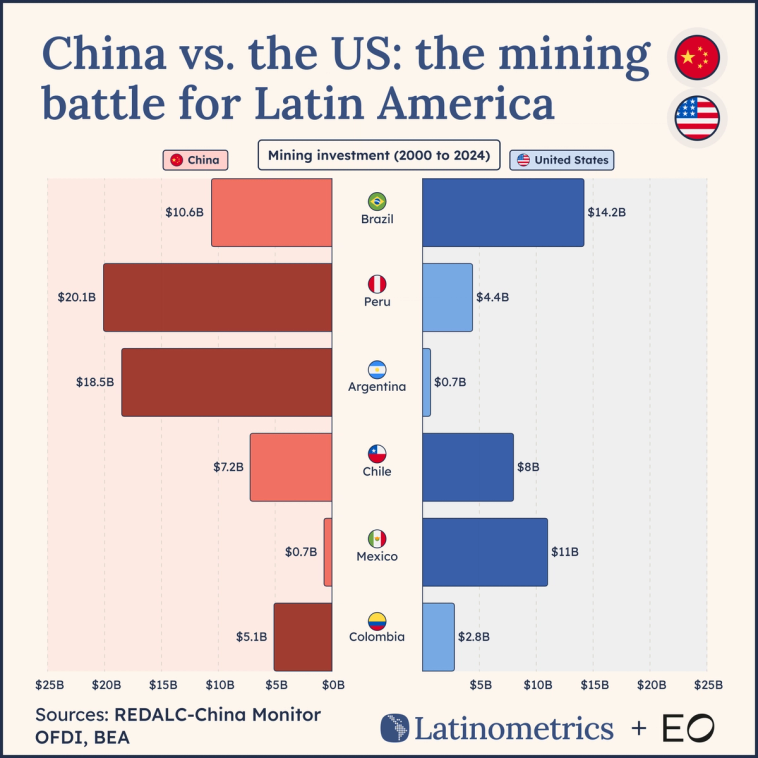

Within the roughly $200B invested in Latin America by Chinese firms since 2000, no sector has been better represented than mining, which managed to attract roughly $72B over this period, reflecting over a third of all Chinese investments regionally.

That Chinese companies like Sinosteel and Zijin Mining are so interested in acquiring or setting up mines across Latin America is far from surprising. After all, centuries after precious metals like gold and silver first attracted Iberian settlers, Latin America's mineral wealth is once more the envy of the land, in particular the critical minerals that are powering the energy transition.

Given China's near-hegemonic position in supply chains for the current processing and refining of minerals such as rare earths, the US is seeking to assert itself within Latin America to build its own alternative supplies. This has involved strategic alliances with countries like Argentina, Brazil, Ecuador, Paraguay, and more.

There's lots of road to catch up on. Despite the US being both a larger economy and larger overall investor, its companies have fallen behind in terms of mining investments since the turn of the century.

Notably, in overall investment terms US companies have eked out a lead in Chile and maintained their dominance in the region's two largest economies of Brazil and Mexico. However, in Andean countries like Argentina and Peru, even stalwart US allies like Colombia, Chinese mining companies have far outperformed, in the Argentine case to the tune of over $16B more.

The Trump administration's strategic partnerships and activity by the recently re-energized Development Finance Corporation (DFC) may play a role in developing US investment in these countries' mining sectors, but more will be needed. In the case of Argentina, rebuilding the trust of foreign firms after decades of mistrust and lengthy nationalization cases will be a necessity—to say nothing of Venezuela, which US firms all but abandoned for years, leaving open to Chinese companies.

Source: REDALC-China Monitor (OFDI)

Still, don't underestimate the important of bilateral ties to critical mineral cooperation, or vice versa. Unlike cases like Chile or Ecuador, Brazil is not an ideological US ally today, nor even a country more dependent on US trade than Chinese trade.

Given Brazil's vast deposits of niobium, tin, manganese, and other critical minerals and rare earths for which it's believed to have the world's second-largest reserves after China, it's clear that South America's giant has the most potential for foreign companies, whether US or Chinese.

Accordingly, even the notably undiplomatic US government has played nice in recent months, bridging ideological and partisan gaps with clear willingness to cooperate on developing Brazil's mineral deposits.

Brazil has already scored over $14B in US mining investments since 2000, but significantly more will be needed if the US hopes to create its own Americas-centric supply chain for the technologies of tomorrow.

Alvaro reminds us that there are huge government employers out there that we may have missed when looking at the region's biggest employers.