📈 Banking Concentration

Which countries have competitive banking landscapes?

If you choose "No" you will no longer receive our finance-focused content. You will still receive all our other newsletters

Yes, keep sending me finance-focused newsletters.

No, remove me from those emails.

Last week, we looked into the revenue models driving Mexico's banks. As we mentioned, Mexico's five largest banks control two-thirds of all national banking assets.

Yet, by Latin-American standards, Mexico’s banking concentration is mild; only Argentina and Panama display more competitive asset shares.

Before we look at how consolidation has shifted over time, it’s worth examining Panama’s banking scenario.

Panama's impressive banking sector is well-regarded globally. The country has the largest international financial center in Central America, with total assets exceeding Panama's GDP by more than double. But only 60% of these assets are held by the country's five largest banks, demonstrating more competitiveness than any other country in Latin America.

On the flip side, we have autocratic countries like Cuba and Nicaragua, where there are a handful of state-owned institutions that run the entire show. Beyond this, we see countries like El Salvador, Peru, and Uruguay, where a number of subsidiaries of foreign banks, such as BBVA and Scotiabank, dominate the local landscape.

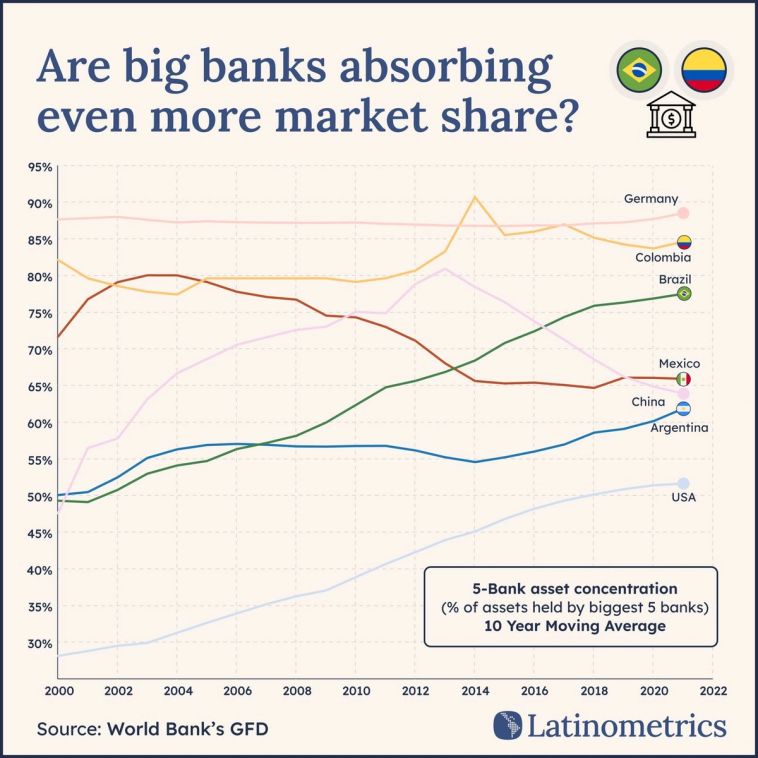

Interestingly, some countries have seen a consolidation process over the last quarter-century despite the Fintech disruptions. Brazil, for example, is home to Latin America's five largest banks: Itaú Unibanco, Banco do Brasil, Bradesco, Caixa, and Santander Brasil. Since 2000, these major players have shifted from holding half of all Brazilian assets to nearly 80%, resulting in a financial landscape in Brazil that is more concentrated than ever today.

As of last year, these five banks held over $1.8 trillion in assets—equivalent to more than 75% of Brazil's GDP.

Notably, this concentration comes as Argentina and Colombia have generally maintained consistent levels of competitiveness in their banking sectors. In contrast, Mexico's banking sector has become more diversified.

All of these cases fall within the range of the United States (with a 5-bank asset concentration of roughly 50%) and Germany (with nearly 90%).

Fernando attributes Chile’s rise in solar power to his country’s good policy